Withdrawal & Investment Strategies

Part 8: I know how much I want, but how do I go about getting it week to week?

Sequencing Risk Part 1

The System is Designed to Fail

In this article we explain:

Why the Default Superannuation System is designed to fail retirees because of Sequencing Risk

An example of the Magnitude that this risk poses to retirees

Potential solutions

The Default Superannuation System is designed to fail retirees

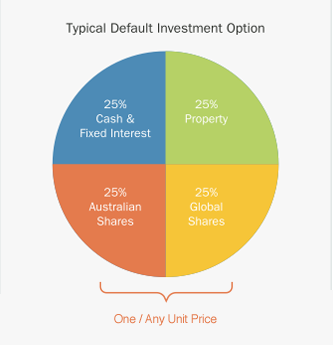

If you have not actively gone out of your way to change the investment strategy in your super fund you will be in the default investment option which for most super funds looks something broadly like this:

The money in the Typical Default Investment Option is spread out across the various major asset classes in a percentage broadly based on our example above. So by investing in this option you are actually investing:

25% of your money in cash and fixed interest, 25% into Property, 25% into global shares and 25% into Australian shares.

The underlying price of these assets is combined into one single price called a UNIT PRICE.

You would have seen this on your superannuation statement before: You currently have 10,000 units in the Balanced fund and the current unit price is 12.50 therefore, your balance is $125,000.

Over time as the value of the shares and properties go up and down the value of the unit price changes accordingly. When you put money into your super fund, you buy more units at the price on that day.

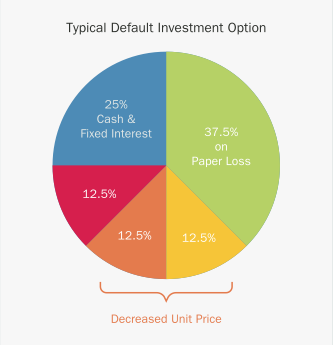

Now consider a scenario similar to the Global Financial Crisis when Share Markets and Global Property markets fell by around 50%.

Now, what if you made this loss real in dollar terms? If you start withdrawing money from your super at retirement, you are now selling your units at a loss!

As you can see, the value of your cash and term deposits have remained unchanged. However, the values of your shares and properties have significantly reduced. Given all your assets have ONE combined unit price; the entire value of your superannuation would have reduced on paper.